28th May 2026

SEA-LNG’s Reflections on MEPC 84

Photograph: MEPC84 session taken by IMO

by Steve Esau, Chief Operating Officer, SEA-LNG:

The discussions at MEPC 84 demonstrated that the IMO’s decarbonisation process is back into an active political negotiation phase. While there is broad support for the 2023 IMO GHG Strategy and for maintaining a global framework for shipping decarbonisation, the pathway towards agreement on the IMO Net-Zero Framework (NZF) is now significantly more open and uncertain.

For industry, this matters.

What emerged clearly during MEPC 84 was that the debate is no longer centred on whether the IMO should establish a global framework for maritime decarbonisation. There is broad alignment on that objective. The challenge now is achieving convergence on what a globally acceptable framework should look like in practice, particularly regarding the balance between environmental ambition, economic impacts, fuel availability, infrastructure readiness and political acceptability.

In these respects, MEPC 84 marked a recognition that compromise remains necessary if the IMO is to preserve its role as the central global regulator for shipping decarbonisation.

One global framework remains essential

One of the clearest areas of alignment throughout the discussions was the importance of maintaining the IMO as the primary global regulator. This is a crucially successful outcome from MEPC 84 for SEA-LNG members. Delegations repeatedly warned that failure to achieve convergence could accelerate the development of regional and unilateral measures, increase fragmentation and expose shipping to overlapping compliance regimes and duplicated costs.

For industry stakeholders, the risks associated with fragmentation are considerable. Shipping is a global industry requiring globally workable solutions. Investment decisions involving vessels, fuel infrastructure and supply chains are made over decades, not political cycles. Regulatory divergence creates uncertainty that directly impacts investment timing, fleet renewal and fuel-transition strategies.

The discussions reinforced the need for a single global framework that is goal-based, technology neutral and capable of accommodating different transition pathways while maintaining environmental integrity.

From technical process to political negotiation

Much of the technical work surrounding implementation guidelines, lifecycle assessment methodologies and supporting frameworks continued at MEPC 84. However, the political discussions focused on the architecture of the NZF itself.

This became particularly visible during negotiations on the Terms of Reference for ISWG-GHG 22 and 23. What might otherwise have been procedural discussions effectively became proxy negotiations on whether – and to what extent – the NZF remains open for renegotiation.

The outcome was significant.

The agreed Terms of Reference ultimately kept all major options on the table, allowing for further consideration of proposals seeking limited refinements to the existing framework. They include concerns relating to the current MARPOL Annex VI amendments, continued development of implementation guidelines and lifecycle assessment methodologies, as well as proposals involving broader structural changes to the framework itself. As a result, the process has shifted away from what had appeared to be a near-adoption phase at MEPC Extraordinary meeting (ES.2) in October 2025. The NZF is now back within a broader political negotiation process.

These discussions increasingly reflect the commercial realities now facing the maritime sector. Decarbonisation pathways must not only be environmentally credible, they must also be practical, scalable and investable. Regulatory frameworks that move faster than fuel supply chains, infrastructure development or commercially available technologies risk undermining both confidence and implementation. Taxing the industry without delivering any reduction in GHG emissions.

This is particularly important for first movers that have already invested heavily in lower-emission technologies and fuel pathways. Regulatory certainty and flexibility remain essential if industry is to continue investing at the scale required to support the transition.

The key role of transition pathways

The discussions also reflected growing recognition that transition pathways will remain necessary as the industry moves towards long-term net-zero objectives.

Concerns regarding fuel availability and infrastructure readiness featured prominently throughout the debates, alongside broader discussions around energy security, trade competitiveness and impacts on developing economies.

Fuel decarbonisation pathways that can deliver immediate emissions reductions while maintaining scalability and commercial viability are likely to remain central to the debate as negotiations continue.

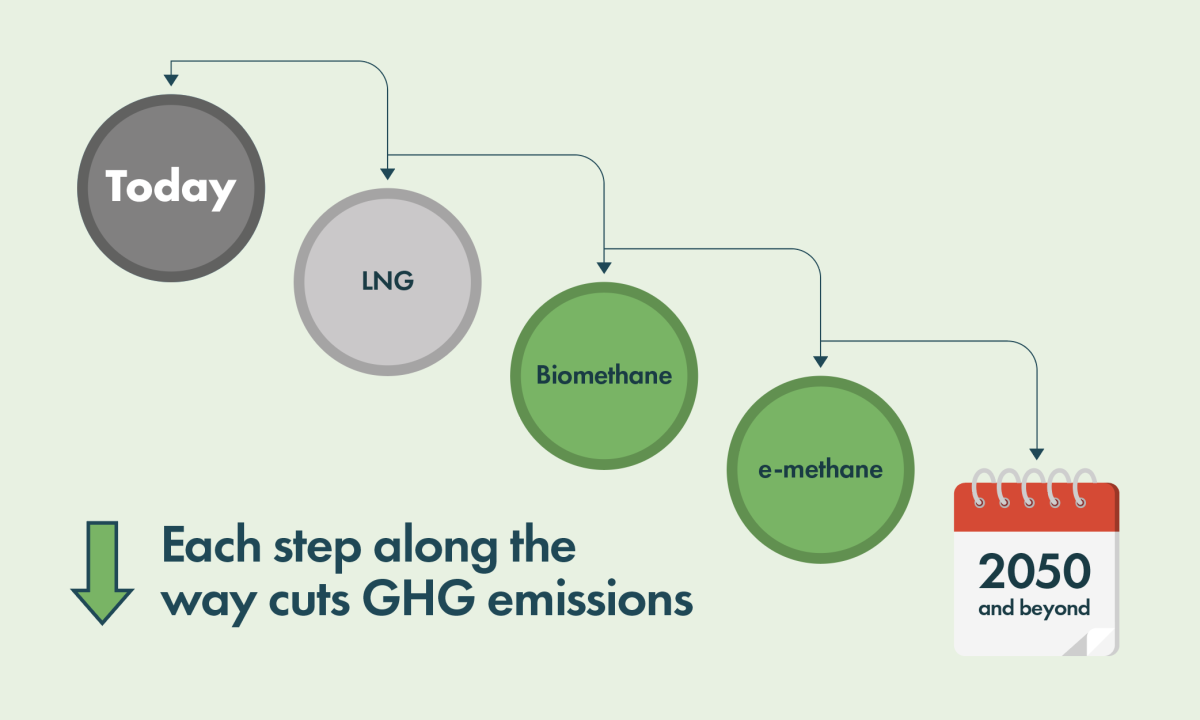

The methane decarbonisation pathway, from LNG through liquefied biomethane and ultimately e-methane, continues to demonstrate many of these characteristics, particularly in relation to infrastructure readiness, fuel availability and optionality. Rapidly increasing biomethane bunkering activity, especially in Europe, and ongoing investment in e-methane development further illustrate how existing fuel pathways can continue evolving alongside tightening regulatory requirements.

The economic mechanism remains a critical matter

MEPC 84 also reinforced that discussions around the NZF are no longer purely technical or environmental, but increasingly shaped by broader geopolitical and economic considerations. Just and equitable transition and differing national circumstances remained central themes throughout the negotiations, particularly regarding the economic element and the proposed Net-Zero Fund. For many developing countries, these mechanisms are seen as politically essential to support transition efforts and mitigate economic impacts, while others continue to express strong concerns regarding the practicality and acceptability of measures perceived as global carbon pricing. Reconciling these differing priorities will now become one of the central challenges of the next phase of negotiations.

The next steps

The agreement to hold further intersessional negotiations before MEPC 85 confirms that additional time will be needed to build broader convergence around the future shape of the NZF. While several pathways remain possible, ranging from limited refinements to more substantial redesign of the framework, the discussions at MEPC 84 demonstrated that consensus on the final structure, economic architecture and implementation pathway has not yet been achieved.

At this stage, adoption of amendments during the resumed extraordinary session in December will be challenging. However, if meaningful progress and political convergence can be achieved during the upcoming intersessional negotiations, there remains a possibility that a revised framework could still be brought forward for approval and later adoption in 2027.

What remains clear is that industry requires a framework capable of balancing ambition with realism. The coming negotiations will therefore be critical not only for the future shape and credibility of the NZF itself, but also for maintaining confidence in the IMO’s ability to deliver a practical, scalable and globally acceptable decarbonisation framework for international shipping.

Our position

SEA-LNG remains clear in its view that:

- There should be a single global decarbonisation framework for maritime. This should be set by the IMO, and all Member States should act accordingly, any local or regional regulations should converge with IMO regulations, with no double compliance costs.

- Any future IMO regulations should be goal-based and technology-neutral, without being prescriptive towards any given decarbonisation pathway.

- Regulations should incentivise solutions that are practical, scalable and investable given current technologies and realistic technology pathways, and which leverage existing infrastructure.